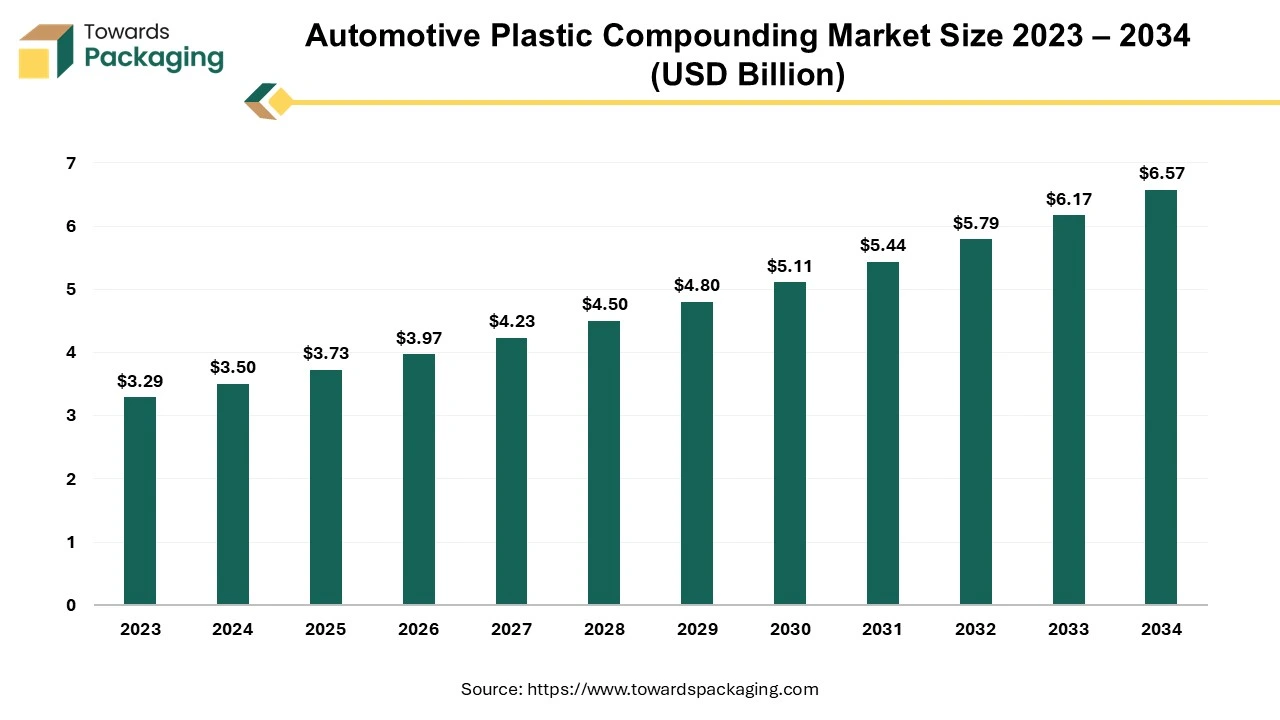

The automotive plastic compounding market is forecasted to expand from USD 3.97 billion in 2026 to USD 7.00 billion by 2035, growing at a CAGR of 6.50% from 2026 to 2035. The Automotive Plastic Compounding Market study includes market size and forecast to 2035, Asia Pacific dominance, fastest growth in North America, detailed segment data by polypropylene, polycarbonate and applications, plus trade data, value chain structure, manufacturer and supplier analysis, and competitive positioning of key global players.

The key players operating in the market are focused on adopting inorganic growth strategies like acquisition and merger to develop advance technology for manufacturing automotive plastic compounding which is estimated to drive the global automotive plastic compounding market over the forecast period.

Automotive plastic compounding means the process of customizing and improving plastic materials to meet the specific requirements of automotive applications. This involves blending base polymers (like polypropylene, polycarbonate, or ABS) with additives, fillers, reinforcements, and colorants to improve the material's properties.

The automotive plastic compounding designs plastics to meet requirements such as strength, durability, heat resistance, or aesthetics. The automotive plastic compounding can improve flowability or reduce cycle times during molding. In summary, automotive plastic compounding ensures that the plastic materials used in vehicles meet performance, regulatory, and aesthetic standards.

Companies are focusing on using recycled and bio-based materials to meet sustainability goals. For instance, mechanically recycled plastic compounds and bio-based polyamides are gaining traction in automotive applications.

Innovations in plastic compounding, such as nanocomposites and advanced polymer blends, are enabling enhanced performance in terms of mechanical strength, heat resistance, and durability, catering to stringent automotive standards.

Automotive manufacturers are leveraging plastic compounding for customized solutions that offer superior aesthetics, aerodynamic properties, and safety features. This includes UV resistance, color matching, and flame retardancy.

Integrating AI into the automotive plastic compounding industry offers numerous benefits by enhancing sustainability, innovation and efficiency. The artificial integration can analyze large datasets to predict the best combinations of polymers and additives for specific automotive applications, durability, optimizing strength, and lightweight properties. Machine learning models can predict how different compounds will perform under various conditions, minimizing the need for extensive physical testing.

The integration of artificial intelligence predictive analytics can detect defects in compounded materials more accurately than traditional methods, ensuring higher quality standards. Automated inspection systems can monitor production in real-time, identifying inconsistencies early in the process.

The emergence of electric vehicles increases the demand for advanced materials that offer lightweight properties, heat resistance, and durability for components like battery casings and thermal management systems. The growth in the sales of the electric vehicles has risen the demand for automotive plastic compounding, which has estimated to drive the growth of the automotive plastic compounding market over the forecast period.

Electric vehicles manufacturers are looking for recyclable and sustainable materials to align with environmental goals. Advances in compounding techniques allow the integration of recycled content into automotive-grade plastics. The expansion of electric vehicles infrastructure drives demand for plastic compounds in charging station components, such as enclosures and connectors.

According to data from the Vahan Dashboard, sales of electric vehicles (EVs) in India decreased month over month in the majority of categories in November 2024 as compared to October 2024. E-rickshaws plummeted 8.2% to 40,386 units, while electric two-wheelers (E2W) fell 14.9% to 118,944 units.

While E-Carts fell 7.9% to 5,423 units and Electric Three-Wheelers (L5 Cargo/Goods) fell 11.2% to 2,251 units, the only category to see growth was Electric Three-Wheelers (L5 Passenger), which increased 3.9% to 15,355 units. Electric buses fell precipitously by 59.5% to 161 units, while electric four-wheelers (E4W) suffered a notable reduction of 22.9% to 8,613 units.

The key players operating in the market facing issue in fulfilling environmental regulations and competition from alternative material, which may restrict the growth of the automotive plastic compounding market. High costs of specialized polymers and additives, such as high-performance engineering plastics and flame retardants, can limit their adoption, especially in cost-sensitive markets. The upfront cost of transitioning from traditional materials like metal to plastic compounds can deter smaller manufacturers.

Some compounded plastics, particularly those with multi-material blends or added reinforcements, are difficult to recycle, raising concerns about end-of-life disposal and environmental impact. Inadequate recycling systems in many regions hinder the industry's ability to meet sustainability demands. Governments worldwide are enforcing stricter regulations on plastic usage and waste, which may limit the growth of certain compounded plastics. Increased focus on bio-based or biodegradable materials could reduce demand for traditional compounded plastics.

In some applications, plastics may still fall short compared to metals in terms of mechanical strength, thermal stability, or fatigue resistance, restricting their use in critical automotive components. Growing competition from lightweight alternatives like advanced alloys, composites, or natural fibers can limit the demand for plastic compounds. Disruptions in the supply of polymers or specialty additives, due to geopolitical issues or natural disasters, can impact production and increase costs.

Increased focus on environmental sustainability is rising demand for recyclable, biodegradable, and bio-based plastic compounds. Opportunities exist in developing compounds that integrate recycled materials while maintaining high performance, aligning with global sustainability goals. Plastic compounds with lower carbon footprints during production and usage are gaining favor among automakers.

The rising in demand for engineering plastics and advanced compounds, such as polycarbonate blends, thermoplastic elastomers (TPEs), and polyphenylene sulfide (PPS), is rising for applications requiring strength, heat resistance, and durability. Incorporating nanotechnology into plastic compounding can enhance properties like stiffness, strength, and thermal resistance, creating opportunities for more sophisticated automotive applications.

| Aspect | Future Focused Insight |

| Market essence | Engineered plastics for vehicles enabling lightweighting, durability, and heat resistance; used in interiors, bumpers, under-the-hood parts, and E components. |

| Future challenges |

|

| Regional outlook |

|

| Future opportunities |

|

| Strategic takeaway | Focus on sustainable, lightweight, and high-performance plastics to capture EV & hybrid growth; regional strategy is key for competitive advantage |

The polypropylene segment held a dominant presence in the automotive plastic compounding market in 2025. polypropylene is one of the lightest polymers, significantly reducing the weight of automotive components, which improves fuel efficiency in traditional vehicles and extends battery range in electric vehicles (EVs). Polypropylene is utilized for door panels, dashboards, trims, and consoles due to its durability, aesthetic appeal, and customization options.

Polypropylene provides an excellent balance of stiffness and impact resistance, making it suitable for both rigid and semi-flexible applications. It offers long-term durability, maintaining its performance under varying environmental conditions.

Polypropylene's combination of mechanical properties, cost-effectiveness, lightweight, and versatility makes it indispensable in automotive plastic compounding. It meets the industry's requirements for design flexibility, durability, and sustainability, ensuring its continued dominance in automotive applications.

The polycarbonate (PC) segment is expected to grow at the fastest rate in the automotive plastic compounding market during the forecast period of 2026 to 2035. Polycarbonate is highly resistant to impact, making it ideal for automotive parts like bumpers, dashboards, and protective shields, which require durability and crash resistance.

Cutting-down vehicle weight is crucial for improving fuel efficiency and meeting emissions standards. Polycarbonate is much lighter than glass and metals, helping manufacturers achieve these goals. Polycarbonate's insulating properties are beneficial for the growing trend of electric vehicles (EVs), where safety in managing electrical components is crucial.

The interior segment registered its dominance over the global automotive plastic compounding market in 2025. Luxury car buyers expect high-quality, visually appealing interiors. Automotive plastics, especially those with advanced finishes, textures, and colors, allow for greater design flexibility compared to traditional materials like wood or metal. Plastics can be molded into complex shapes and combined with coatings to create high-end aesthetics, such as gloss, matte, or metallic finishes.

Luxury cars are increasingly integrating high-tech features like touchscreens, wireless charging stations, ambient lighting, and advanced climate control systems. Plastic materials are crucial for the housing and support of these electronic components. The ability of plastics to be molded with precision allows designers to incorporate intricate shapes and seamless interfaces for a modern, high-tech interior.

The growing demand for luxury car interiors is pushing the need for automotive plastic compounding because plastics offer the ideal combination of aesthetic flexibility, lightweight performance, durability, advanced functionality, and sustainability attributes highly valued in the luxury automotive sector.

Asia Pacific region dominated the global automotive plastic compounding market in 2025. Governments in the region, particularly in China, Japan, and South Korea, provide incentives for electric vehicle adoption. This includes subsidies and mandates for lightweight, fuel-efficient vehicles, indirectly promoting the use of plastic compounds in automotive applications.

The Asia-Pacific region has a well-established supply chain for both EV production and plastic compounding, including raw material availability and processing capabilities, making it easier for manufacturers to source and integrate advanced plastic compounds.

The close collaboration between EV manufacturers and the plastic compounding industry in the Asia-Pacific region fosters innovation and rapid product development, further strengthening both sectors. Asia-Pacific's EV market is a leader in innovation, with manufacturers frequently designing new models that require advanced materials for batteries, interiors, exteriors, and thermal management. Local plastic compounders benefit by developing specialized materials tailored to these needs.

China plays a distinctive role in supporting the automotive plastic compounding market through its dominance in the EV industry. Its rapid EV adoption and production, coupled with its global leadership in battery technology, fuels the demand for lighter, more fuel-efficient materials like plastic compounds. Furthermore, the dominance of China in battery technology, particularly in lithium-ion batteries and sodium-ion batteries, spurs the necessity for lighter and more efficient vehicle components made from plastic compounds.

Japan is also experiencing growth in the EV market, which contributes to the trend through its EV production and commitment to zero-emission goals, further increasing the demand for automotive plastic compounds. Japanese automakers are actively developing and launching new EV models, which fosters the demand for lighter and more fuel-efficient materials like plastic compounds. Moreover, the minicar market of Japan, comprising small, affordable EVs, also contributes to the need for plastic compounds, as these vehicles often utilize lighter and more efficient materials.

North America region is anticipated to grow at the fastest rate in the automotive plastic compounding market during the forecast period. Automakers are under pressure to improve fuel efficiency and reduce emissions. Plastics are replacing traditional materials like metal because they offer weight savings without compromising strength or durability.

Government regulations, such as the Corporate Average Fuel Economy (CAFE) standards in the U.S., are further accelerating the adoption of lightweight materials. Key players in North America are heavily investing in research to create high-performance compounds that cater to the growing demand for advanced automotive applications. Despite fluctuations, North America remains a significant hub for automotive production, creating consistent demand for high-quality plastic materials.

The U.S. plays a distinct role in the automotive plastic compounding market. This is primarily driven by its robust automotive manufacturing sector, with major players like General Motors, Ford, and Tesla, and growing adoption of advanced technologies and sustainable practices. Furthermore, the focus on lightweight materials for fuel efficiency and compliance with environmental regulations by country contributes to the demand for specialized plastic compounds in vehicle production. Additionally, the trend towards electric vehicles and autonomous technologies further fuels the demand for such materials in various automotive applications.

The MEA automotive plastic compounding market is growing because of the growing demand for lightweight vehicles and automobile production. Utilizing engineering plastics lowers vehicle emissions and increases fuel economy. Government programs to support regional auto production encourage market growth. However, rapid growth is constrained by expensive raw materials and constrained local supply chains.

In the UAE, the demand for luxury cars and rising car sales are driving up the use of plastics. To increase vehicle efficiency, high-performance and lightweight materials are used. The market for engineering plastics is further increased by investments in electric and hybrid vehicles. Advanced applications are made possible by access to imported materials and a robust infrastructure.

The Latin American market is expanding because of an increase in the production and export of cars. Plastic compounds assist automobiles in meeting safety and lightweight regulations. Demand is further supported by the growing use of EVs and contemporary vehicle designs. Countries with high reliance on imports and low domestic production capacity see slower market growth.

Brazil

Brazil is the largest automotive plastic compounding market in Latin America due to its strong automobile industry's use of polymers for interior, bumpers, and under the hood component sis, increasing government policies promoting local automotive manufacturing support market development. Rising demand for lightweight and sustainable vehicles further drives growth.

This market relies on engineering plastics and polymer additives to meet strength, durability, and lightweight requirements.

Key players: BASF, SABIC, Covestro, LyondellBasell.

Close coordination with automotive OEMs and Tier-1 suppliers ensures timely material delivery and production efficiency.

Key players: BASF, LANXESS, Celanese.

Recyclable and bio-based compounds are gaining traction to meet automotive sustainability targets.

Key players: BASF, SABIC, DSM Engineering Materials.

By Product

By Application

By Region

Research & Advisory Analyst

Yogesh Kulkarni is an experienced Research Analyst specializing in the packaging sector, with a strong foundation in statistical analysis and market intelligence. He currently contributes his expertise to Towards Packaging.

Learn more about Yogesh Kulkarni

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarAutomotive Plastic Compounding Market