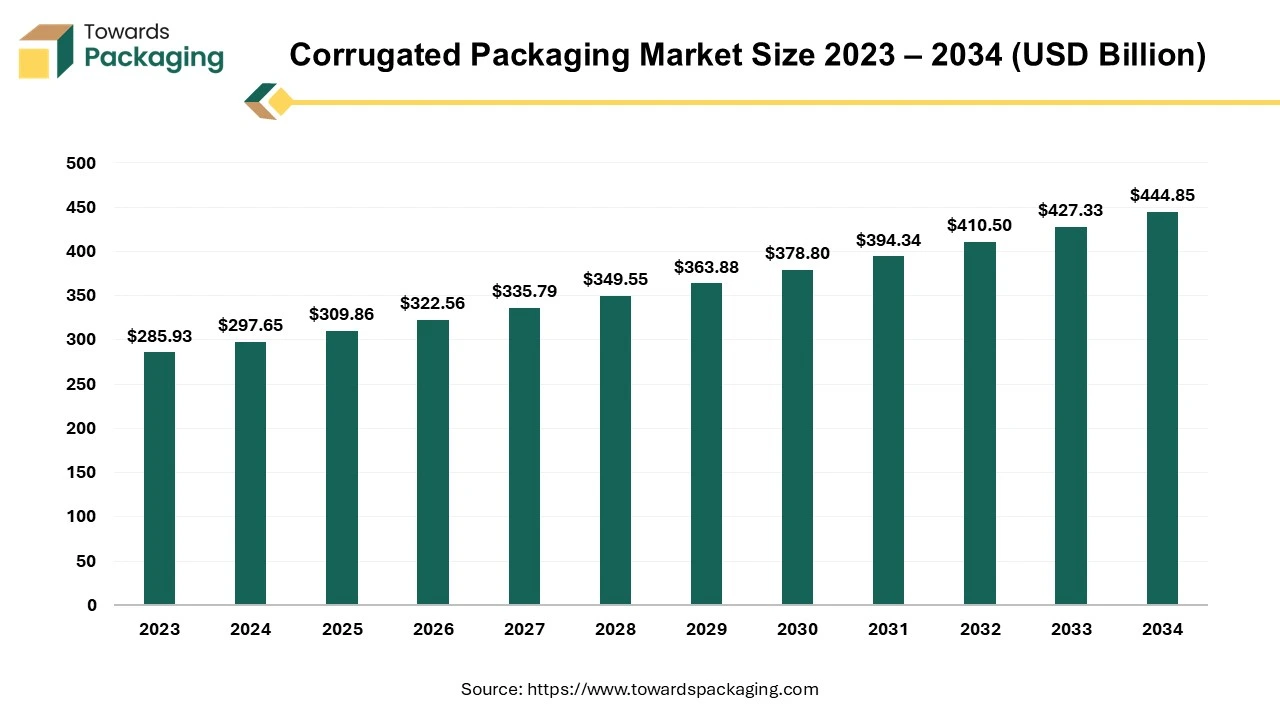

The corrugated packaging market is forecasted to expand from USD 322.56 billion in 2026 to USD 463.09 billion by 2035, growing at a CAGR of 4.1% from 2026 to 2035. This growth is driven by the rise of e-commerce, where corrugated packaging plays a crucial role in product shipping and protection. The market’s expansion is also fueled by the increasing adoption of eco-friendly alternatives, with sustainability becoming a key driver.

Additionally, the growing demand for customized, fit-to-product packaging to optimize logistics and reduce waste is reshaping the industry. Rapid expansion in online retail and the need for sturdy, cost-effective shipping solutions drive strong demand. Growing environmental regulations also push companies to adopt eco-friendly alternatives, fueling market growth.

Corrugated packaging refers to a type of lightweight, durable, and eco-friendly packaging manufactured from corrugated fiberboard, which consists of a fluted (wavy) middle layer sandwiched between two flat linerboards. This structure provides strength, impact resistance, and cushioning, making it ideal for shipping, storage, and product protection. Corrugated fiberboard is made up of three main components: liner board, fluting (Medium), and adhesives. The key benefits of corrugated packaging have been mentioned here as follows: strength, durability, cost-effective, lightweight, and versatility.

| Metric | Details |

| Market Size in 2025 | USD 309.85 Billion |

| Projected Market Size in 2035 | USD 463.09 Billion |

| CAGR (2026 - 2035) | 4.10% |

| Leading Region | Asia Pacific |

| Market Segmentation | By Wall Type, By Packaging Type, By Application and By Region |

| Top Key Players | Mondi Group, WestRock Company, International Paper Company, DS Smith PLC, Smurfit Kappa Group, Nine Dragons Paper (Holdings) Limited |

| Europe Corruagted Packaging Market | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2034 |

| Value (EUR Million) | 79.3 | 82.6 | 86.0 | 89.6 | 93.4 | 97.3 | 101.4 | 105.8 | 110.4 | 115.3 |

| By Country (Value) | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2034 |

| Germany | 16.4 | 17.1 | 17.9 | 18.7 | 19.5 | 20.4 | 21.3 | 22.3 | 23.3 | 24.4 |

| Poland | 4.5 | 4.7 | 4.9 | 5.2 | 5.4 | 5.7 | 6.0 | 6.3 | 6.6 | 6.9 |

| Austria | 2.2 | 2.3 | 2.3 | 2.4 | 2.5 | 2.6 | 2.7 | 2.8 | 2.9 | 3.0 |

| Czech Republic | 1.9 | 1.9 | 2.0 | 2.1 | 2.2 | 2.2 | 2.3 | 2.4 | 2.5 | 2.6 |

| Belgium | 2.6 | 2.7 | 2.8 | 2.9 | 3.0 | 3.1 | 3.3 | 3.4 | 3.5 | 3.6 |

| Netherlands | 3.9 | 4.1 | 4.2 | 4.4 | 4.5 | 4.7 | 4.9 | 5.1 | 5.3 | 5.5 |

| Switzerland | 1.5 | 1.6 | 1.7 | 1.7 | 1.8 | 1.9 | 2.0 | 2.1 | 2.3 | 2.4 |

| Turkey | 2.1 | 2.2 | 2.3 | 2.5 | 2.6 | 2.7 | 2.9 | 3.0 | 3.2 | 3.3 |

| Rest of Europe | 44.3 | 46.0 | 47.9 | 49.8 | 51.8 | 53.9 | 56.1 | 58.5 | 60.9 | 63.5 |

Environmental concerns are driving the industry towards more sustainable practices. Companies are increasingly adopting recyclable materials, reducing waste, and developing biodegradable packaging solutions. For instance, innovations in paper-based packaging and reusable designs are gaining traction, aligning with consumer demand for environmentally friendly products.

The incorporation of smart technologies into corrugated packaging is enhancing supply chain efficiency and customer engagement. Features such as QR codes, RFID tags, and NFC technology enable real-time tracking, authentication, and interactive consumer experiences. This trend is particularly beneficial for inventory management and combating counterfeit products.

Automation is revolutionizing the production of corrugated packaging by improving precision, reducing labor costs, and increasing output. The adoption of advanced machinery and robotics facilitates faster turnaround times and customization capabilities, allowing manufacturers to meet diverse client needs more effectively.

Brands are leveraging customized packaging designs to enhance the unboxing experience and strengthen customer loyalty. Techniques such as die-cut designs and personalized prints not only protect products but also serve as powerful marketing tools, creating memorable interactions with consumers.

| Rank | Manufacturer | Share (%) |

| 1 | International Paper | 7 |

| 2 | WestRock (merged with Smurfit Kappa in 2024; shown separately for 2024) | 5.5 |

| 3 | Smurfit Kappa | 4.8 |

| 4 | Oji Holdings | 4 |

| 5 | Nine Dragons Paper | 3.7 |

| 6 | DS Smith | 3.3 |

| 7 | Mondi | 3.1 |

| 8 | Georgia-Pacific | 2.8 |

| 9 | Lee & Man Paper | 2.4 |

| 10 | Packaging Corporation of America (PCA) | 2.2 |

AI-powered sensors monitor equipment performance, predicting failures before they occur, reducing downtime and maintenance costs. AI-driven robotics optimize cutting, folding, and printing processes, increasing precision and speed in manufacturing. AI detects defects (such as misprints, weak glue bonds, or structural weaknesses) in real time, ensuring high-quality output and reducing waste. AI algorithms predict demand and optimize stock levels, reducing raw material waste and avoiding overproduction. AI analyzes real-time data to optimize delivery routes, reducing fuel consumption and ensuring timely deliveries. AI-enabled RFID and QR codes help track packages in real time, improving supply chain visibility.

The potential application of artificial intelligence (Al) in the paper-to-packaging process presents a game-changing prospect for the sector, particularly with regard to the simplification of intricate computer models. This strategy could transform conventional techniques by allowing Al to identify complex connections between different production parameters and the characteristics of the corrugated board that is produced.

By using Al, producers may learn more about how variables like humidity, temperature, and adhesive concentration during production could affect the finished product. This innovative approach's first step is to use Al to evaluate large datasets that include a variety of industrial characteristics. Al algorithms are skilled at finding correlations and patterns that conventional analysis can miss, especially in machine learning models.

The rise of e-commerce giants (Amazon, Alibaba, Flipkart) has significantly increased demand for durable, lightweight, and cost-effective corrugated boxes for shipping. Corrugated packaging ensures product protection during transit, making it the preferred choice for fragile and perishable items. The shift toward subscription-based delivery models (groceries, pet food, and electronics) is further driving demand. In January 2025, according to the data published by the National e-commerce associations, as of the first three quarters of 2025, retail commerce sales in the United States were US$879.54 billion.

The key players operating in the market are facing issue such as fluctuating raw material prices, environmental regulations & sustainability challenges, which has estimated to restrict the growth of the corrugated packaging market. Governments worldwide are implementing strict environmental regulations on packaging waste and deforestation, impacting production. The need for eco-friendly inks, adhesives, and coatings increases production costs. Companies are facing pressure to reduce carbon footprints, requiring investments in renewable energy and greener production methods.

Corrugated packaging relies on kraft paper and recycled fibers, both of which are subject to price fluctuations due to supply-demand imbalances and environmental regulations. Increased demand for sustainable packaging is driving up the cost of recycled paper and virgin fiber materials. Energy-intensive manufacturing processes further contribute to rising production costs.

Increasing demand for corrugated food packaging in fresh produce, takeout, frozen foods, and ready-to-eat meals. Rising adoption of corrugated packaging in dairy, meat, and seafood due to its moisture resistance and protective properties. Innovations like corrugated insulated boxes for temperature-sensitive foods offer new business opportunities.

The global pharmaceutical industry requires secure, tamper-proof, and eco-friendly packaging solutions. Growth in the medical supplies and diagnostics sector is increasing demand for sterile and durable corrugated packaging. Corrugated fiberboard with anti-microbial coatings presents a new market opportunity in healthcare packaging.

| Growth Factor | Market Strength | Industry Advantage |

| Strong Global Demand Base | Widely used across food & beverages, FMCG, pharmaceuticals, electronics, and industrial sectors. | Ensures consistent and recurring demand worldwide. |

| E-commerce Expansion | Rapid growth in online shopping significantly increases demand for protective shipping boxes. | Continuous volume growth driven by digital retail trends. |

| Essential Product Packaging | Critical for packaging groceries, medicines, and daily-use goods. | Maintains stable demand regardless of economic cycles. |

| High Sustainability Profile | 100% recyclable, biodegradable, and widely recovered material with high recycling rates globally. | Aligns with ESG targets and environmental regulations. |

| Lightweight & High Strength | Excellent strength-to-weight ratio supports stacking and product protection. | Reduces transportation costs while maintaining durability |

| Plastic Replacement Trend | Growing shift from plastic to fiber-based sustainable packaging solutions. | Expands application areas and long-term growth potential. |

| Continuous Innovation | Development of lightweight boards and improved protective designs. | Strengthens competitive positioning and future readiness. |

The Indian government has restricted the use of several single-use plastic products to reduce environmental pollution. This move has increased the demand for eco-friendly alternatives such as corrugated boxes and paper-based packaging, especially in FMCG, food delivery, and e-commerce sectors.

The government promotes domestic manufacturing under the “Make in India” program, offering policy support and investment opportunities in the paper and packaging sector. This initiative strengthens local production capacity and boosts exports of corrugated packaging products.

Foreign Direct Investment is allowed under the automatic route in the paper and packaging industry. This has attracted global players, encouraged technology upgrades, and expanded manufacturing infrastructure in the corrugated packaging market.

Revisions in GST rates on packaging materials have helped reduce cost burdens for manufacturers and end users. Tax rationalization supports MSMEs operating in the corrugated box segment and improves price competitiveness.

The Indian Institute of Packaging, under the Ministry of Commerce, provides research, training, testing, and certification services. This improves packaging standards, promotes innovation, and enhances the quality of corrugated packaging solutions.

The single wall boards to segment held a dominant presence in the corrugated packaging market in 2025. Single-wall corrugated boards are the most widely used type of corrugated packaging due to their lightweight nature, cost-effectiveness, and versatility. Lower material and production costs make single-wall boards the preferred choice for manufacturers and businesses. Compared to double-wall or triple-wall boards, they require less raw material, reducing expenses while maintaining adequate protection. Single-wall corrugated boards are widely used in food & beverage, consumer goods, pharmaceuticals, and electronics.

The boxes packaging type segment accounted for a considerable share of the corrugated packaging market in 2025. Boxes provide shock absorption and cushioning to protect goods from damage during shipping and storage. Boxes can be easily stacked for efficient storage and transportation. The box packaging supports logos, product details, and QR codes for marketing and customer engagement. Box packaging dominates the market due to its durability, cost-efficiency, sustainability, and adaptability across industries. Its growing use in e-commerce, food, electronics, and logistics ensures continued demand.

The food & beverages segment led the global corrugated packaging market. Corrugated packaging is a preferred choice for food and beverage packaging due to its strength, sustainability, and ability to protect perishable goods. The corrugated packaging supports eco-conscious businesses and reduces waste. Online grocery and meal deliveries require sturdy, protective, and customizable packaging. Corrugated pizza boxes, takeout containers, and beverage carriers are widely used in fast food and restaurant deliveries. Right-sized packaging innovations help reduce material waste and optimize shipping.

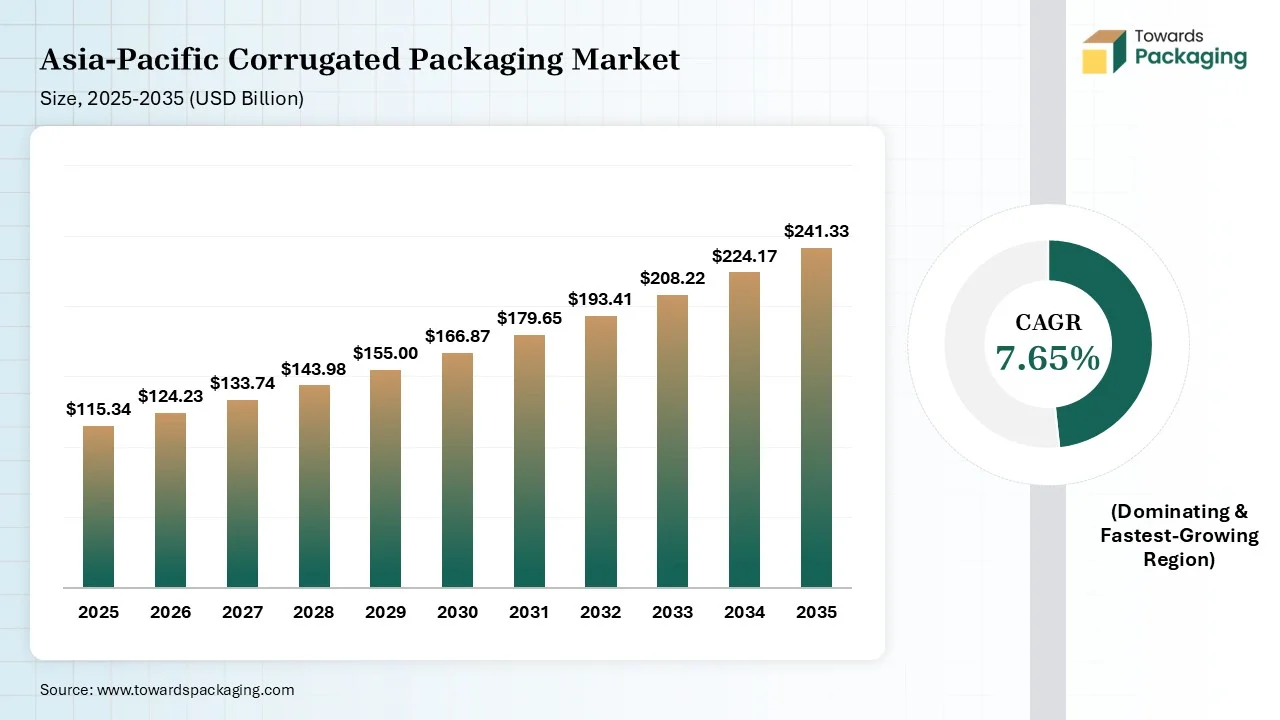

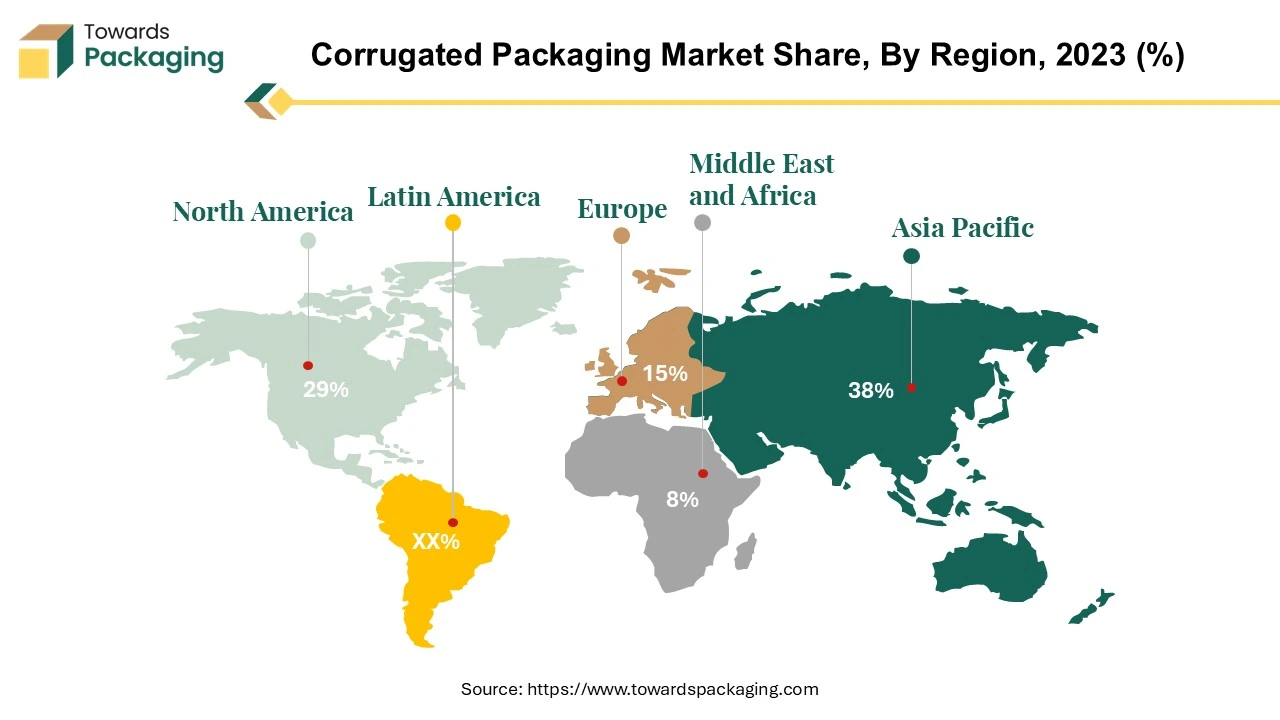

Asia Pacific region dominated the global corrugated packaging market in 2025. APAC has the largest e-commerce market globally, with countries like China, India, Japan, and Southeast Asia experiencing rapid online retail growth. Countries like China, India, Indonesia, and Vietnam are undergoing rapid industrial growth, leading to higher packaging demand in manufacturing, logistics, and exports. Asia Pacific is a global manufacturing hub for industries like electronics, textiles, pharmaceuticals, and automotive, all requiring corrugated packaging for exports. Countries like China, India, Vietnam, and Thailand produce high volumes of corrugated board, cartons, and customized packaging for international markets. APAC companies are investing in automated packaging, AI-driven customization, and smart packaging solutions (RFID, QR codes, IoT-enabled tracking).

")

China Corrugated Packaging Trends

China is the largest producer and consumer of corrugated packaging globally. The market is expanding due to industrial growth, booming e-commerce, government regulations on sustainability, and increasing demand for food and consumer goods packaging. China has the world’s largest e-commerce market, with platforms like Alibaba, JD.com, Pinduoduo, and Douyin (TikTok Shop) driving high demand for durable and customized corrugated packaging.

China remains a global manufacturing hub for industries like electronics, automotive, textiles, pharmaceuticals, and consumer goods, all requiring large volumes of corrugated packaging. China remains a global manufacturing hub for industries like electronics, automotive, textiles, pharmaceuticals, and consumer goods, all requiring large volumes of corrugated packaging. China’s “Plastic Ban 2025” policy is phasing out single-use plastics, boosting demand for eco-friendly corrugated alternatives.

North America is projected to host the fastest-growing corrugated packaging market in the coming years. North America, led by the United States, Canada, and Mexico, is one of the largest and most advanced markets for corrugated packaging. North America has a high e-commerce penetration rate, with giants like Amazon, Walmart, Shopify, and eBay relying heavily on corrugated packaging for shipping and fulfillment. North America has strong domestic production of kraft paper and recycled fiber, ensuring a steady supply of raw materials for corrugated packaging.

")

U.S. Corrugated Packaging Trends

The U.S. has a high online shopping penetration rate, led by Amazon, Walmart, Target, eBay, and Shopify, all relying on corrugated boxes for shipping. U.S. companies are shifting away from plastic due to federal and state bans on single-use plastics (e.g., California’s plastic packaging restrictions). Big brands like Amazon, Walmart, and Unilever are investing in 100% recyclable, compostable, and FSC-certified corrugated packaging. Advances in water-based coatings, biodegradable adhesives, and reusable corrugated packaging are driving sustainability efforts.

Future of North America Corrugated Packaging Market

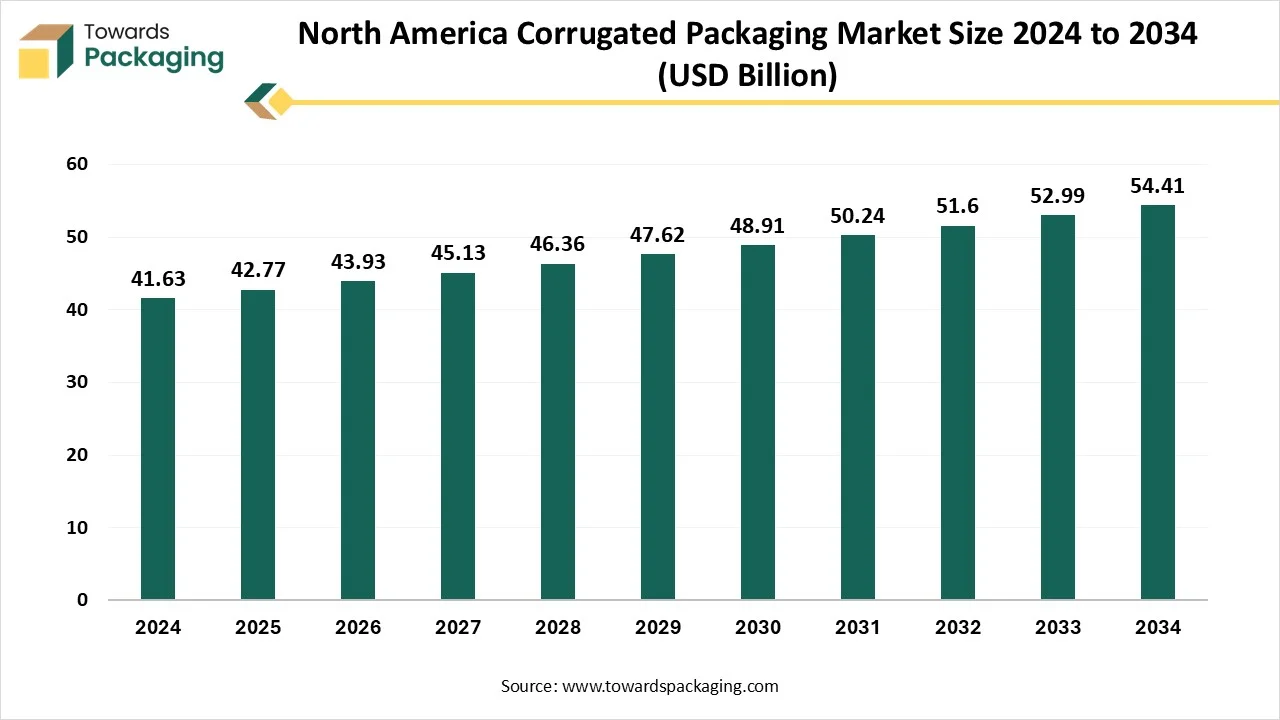

The North America corrugated packaging market is projected to reach USD 54.41 billion by 2034, expanding from USD 42.77 billion in 2025, at an annual growth rate of 2.72% during the forecast period from 2026 to 2035. Processed foods will dominate North America’s corrugated packaging market in the year 2025 due to their widespread consumption and rigid FDA labelling rules and regulations. Corrugated boxes are important for processing fresh produce during transport, especially in the U.S and Canada, where sustainability trade policies and sector assistance further drive market development.

Corrugated packaging is a kind of cardboard material that is made up of three layers: an inside liner, an outside liner, and a fluting corrugated medium sandwiched between the liner sheets. The fluting corrugated medium is generally made of kraft paper, which is rigid and more durable than regular paper. Corrugated containers remain stable even when exposed to moisture, shocks, and sudden temperature fluctuations. While no container is discreet to extreme force or prolonged or rigid conditions, corrugated serves a great level of assurance that our products will shift from our warehouse to their final point in great shape.

")

Europe region is seen to grow at a notable rate in the foreseeable future. The European Green Deal & Circular Economy Action Plan promote recyclable, biodegradable, and reusable packaging. EU Single-Use Plastics Directive (SUPD) is banning plastic packaging, increasing demand for corrugated alternatives. Europe is a global leader in automotive, electronics, pharmaceuticals, and machinery production, requiring heavy-duty corrugated packaging for exports.

| Country | Trade Flow | Trade Value (US$) | Net Weight (kg) | Quantity (kg) |

| Argentina | M | $13,189,650 | 6,469,296.60 | 6,469,297 |

| Argentina | X | $13,016,153 | 9,977,004.50 | 9,977,005 |

| Brazil | M | $44,775,654 | 15,575,524.30 | 15,575,524 |

| Brazil | X | $36,857,005 | 31,358,095.30 | 31,324,159 |

| Colombia | M | $5,124,053 | 1,691,216.10 | 1,691,216 |

| Colombia | X | $9,409,607 | 7,029,687.40 | 7,029,687 |

| Country | Trade Flow | Trade Value (US$) | Net Weight (kg) | Quantity (kg) |

| Australia | M | $91,782,039 | 45,271,960.80 | 45,271,961 |

| Australia | X | $5,989,719 | 10,087,620 | 10,087,620 |

| China | M | $27,748,762 | 5,698,137.70 | 5,698,138 |

| China | X | $1,553,371,837 | 689,417,307.50 | 689,417,308 |

| Sri Lanka | M | $4,110,343 | 1,886,645.50 | 1,886,645 |

| Sri Lanka | X | $13,728,757 | 5,039,734.80 | 5,039,735 |

| India | M | $32,952,906 | 10,810,037.10 | 10,810,037 |

| India | X | $55,789,995 | 38,399,014.90 | 38,399,015 |

| Malaysia | M | $69,357,353 | 36,112,165.80 | 36,112,166 |

| Malaysia | X | $74,875,031 | 47,136,610.30 | 47,136,610 |

| Country | Trade Flow | Trade Value (US$) | Net Weight (kg) | Quantity (kg) |

| Belgium | M | $326,013,482 | 213,513,453.70 | 213,513,454 |

| Belgium | X | $244,109,185 | 176,726,989.50 | 176,726,989 |

| France | M | $578,183,203 | 349,689,757 | 349,689,757 |

| France | X | $231,799,062 | 0 | 0 |

| Germany | M | $568,272,275 | 0 | 0 |

| Germany | X | $1,218,280,031 | 807,330,574.10 | 807,330,574 |

| Italy | M | $97,450,353 | 34,735,239.80 | 34,735,240 |

| Italy | X | $468,861,118 | 0 | 0 |

| Netherlands | M | $852,646,541 | 1,010,697,743 | 1,010,697,743 |

| Netherlands | X | $332,348,774 | 195,425,455 | 195,425,455 |

| United Kingdom | M | $331,131,467 | 0 | 0 |

| United Kingdom | X | $187,934,181 | 0 | 0 |

| Country | Trade Flow | Trade Value (US$) | Net Weight (kg) | Quantity (kg) |

| Israel | M | $16,170,000 | 6,553,493.80 | 6,553,494 |

| Israel | X | $16,161,000 | 7,839,285.30 | 7,839,285 |

| Saudi Arabia | M | $88,399,655 | 0 | 0 |

| Saudi Arabia | X | $216,770,067 | 72,508,673 | 72,508,673 |

| Turkey | M | $20,274,719 | 9,417,195 | 9,417,195 |

| Turkey | X | $323,249,943 | 248,118,837 | 248,118,837 |

| Country | Trade Flow | Trade Value (US$) | Net Weight (kg) | Quantity (kg) |

| Egypt | M | $23,886,273 | 10,270,822.30 | 10,270,822 |

| Egypt | X | $61,098,956 | 32,280,136.70 | 32,280,137 |

| South Africa | M | $13,193,274 | 0 | 5,672,956 |

| South Africa | X | $71,581,689 | 37,818,432 | 37,818,432 |

| Country | Trade Flow | Trade Value (US$) | Net Weight (kg) | Quantity (kg) |

| China, Hong Kong SAR | M | $93,569,089 | 80,883,078 | 80,883,078 |

| China, Hong Kong SAR | X | $20,445,241 | 3,655,815 | 3,655,815 |

| China, Macao SAR | M | $760,534 | 579,971.30 | 579,971 |

| China, Macao SAR | X | $2,062 | 1,382 | 1,382 |

| New Zealand | M | $18,896,716 | 0 | 8,125,370 |

| New Zealand | X | $716,555 | 0 | 378,575 |

| Country | Trade Flow | Trade Value (US$) | Net Weight (kg) | Quantity (kg) |

| Canada | M | $577,474,900 | 287,684,093.30 | 287,684,093 |

| Canada | X | $223,335,445 | 117,993,810.80 | 117,993,811 |

| USA | M | $747,203,934 | 344,218,154.50 | 344,218,155 |

| USA | X | $1,383,886,590 | 0 | 669,498,165 |

| Country | Trade Flow | Trade Value (US$) | Net Weight (kg) | Quantity (kg) |

| Mexico | M | $788,089,384 | 402,922,834 | 402,922,834 |

| Mexico | X | $319,691,638 | 555,192,081.20 | 555,192,081 |

| Country | Trade Flow | Trade Value (US$) | Net Weight (kg) | Quantity (kg) |

| Hungary | M | $204,476,527 | 116,267,751.80 | 116,267,752 |

| Hungary | X | $196,570,130 | 112,325,021.70 | 112,325,022 |

| Ukraine | M | $20,539,684 | 9,187,597.90 | 9,187,598 |

| Ukraine | X | $6,461,734 | 4,947,481.30 | 4,947,481 |

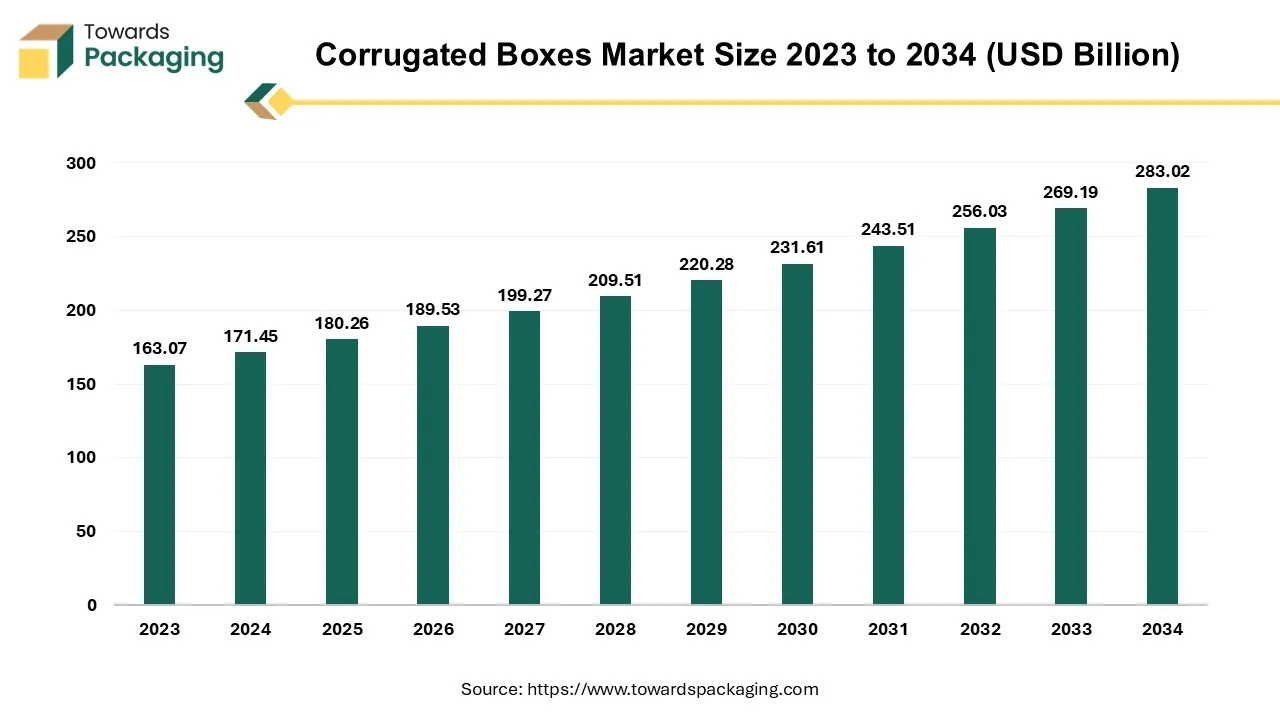

The global corrugated boxes market is projected to reach USD 283.02 billion by 2034, expanding from USD 180.26 billion in 2025, at an annual growth rate of 5.14% during the forecast period from 2026 to 2035. Increasing trend towards sustainable packaging is significant factor anticipated to drive the growth of the corrugated boxes market over the forecast period.

A corrugated box is a disposable container with three layers of material on its sides an outside layer, an inner layer, and a middle layer. When weighted materials are placed inside a corrugated box, the intermediate layer, which is fluted is designed in stiff, wave-shaped arches that act as supports and cushions. The process of aligning corrugated plastic or fiberboard (also known as corrugated cardboard) design elements with the functional, processing, and end-use requirements is known as corrugated box design. Packaging engineers strive to keep overall system costs under control while satisfying a box's performance criteria.

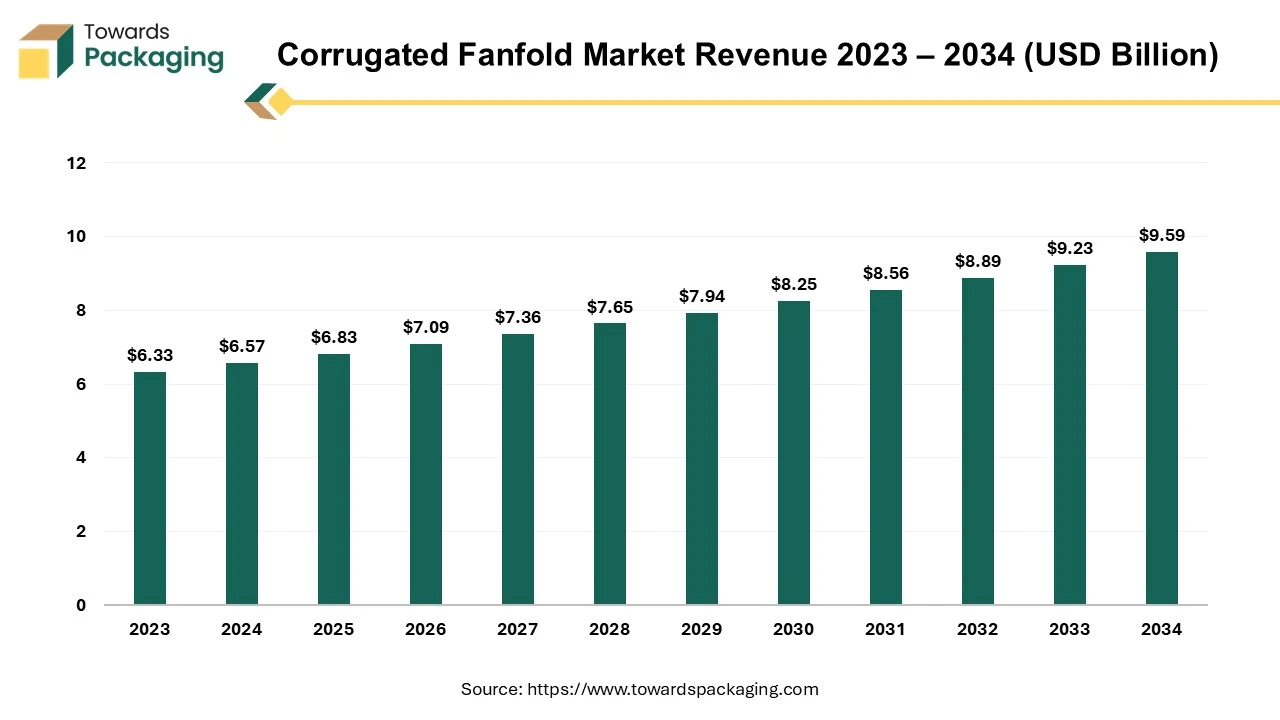

The global corrugated fanfold market is expected to grow from USD 6.83 billion in 2025 to USD 9.59 billion by 2034, registering a compound annual growth rate (CAGR) of 3.85% during the forecast period. This market expansion is primarily attributed to the rising demand for sustainable, cost-efficient, and customizable packaging particularly across e-commerce, logistics, and retail sectors. According to Smithers, the increasing shift toward on-demand packaging and right-sizing solutions continues to drive the adoption of corrugated fanfold among packaging manufacturers.

The market proliferates due to the rising e-commerce sector and the requirement of shipping & logistics where the safe and durable packaging of products is required. There is an increasing demand for sustainable packaging among consumers and strict government guidelines result in the growth of corrugated fanfold market development.

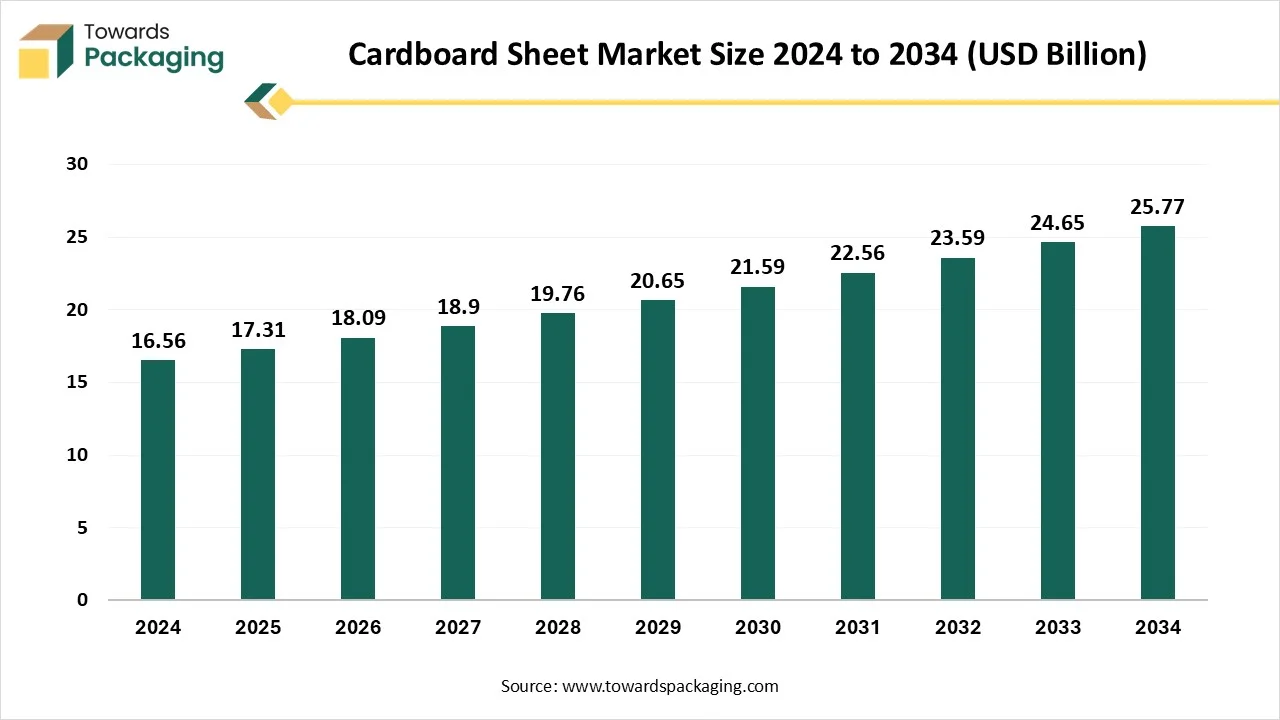

The global cardboard sheet market is forecast to grow from USD 17.31 billion in 2025 to USD 25.77 billion by 2034, driven by a CAGR of 4.53% from 2026 to 2035. The rising demand for sustainable packaging in several industries is due to growing ecological concerns. The increasing e-commerce industry and protective packaging have influenced the growth of the market due to their recyclability, versatility, and cost-effectiveness.

The cardboard sheet market is facing significant development because of the growing demand in the packaging sector. These cardboard sheets are extensively utilised by the retail, e-commerce, and food and beverages sectors due to their eco-friendly and cost-effectiveness nature. The increasing shift in the direction of sustainable packaging options is the major reason behind the growth of the cardboard sheet sector. As a consequence, companies are concentrating on the rise of lightweight, recyclable, and biodegradable cardboard sheets. Moreover, the rising online shopping trend and home delivery services have made a huge contribution to the development of cardboard sheets packaging. The continuous innovation in the production procedure causes the enhancement of the quality and decreases the charges, which supports the market to rise.

Investment focuses on lightweight, high-strength, and eco-friendly corrugated boards. Smart printing and water-resistant coatings are also being developed.

Key Players: International Paper, DS Smith, Smurfit Kappa, Georgia-Pacific, WestRock

Corrugated boxes are optimized for transport efficiency and stacking strength. Integration with e-commerce and retail logistics is a key trend.

Key Players: DS Smith, Smurfit Kappa, WestRock, International Paper, Packaging Corporation of America

Corrugated packaging is highly recyclable, and companies promote waste recovery programs. Recycled fiber content is increasing in production to minimize environmental impact.

Key Players: Smurfit Kappa, WestRock, International Paper, DS Smith, Georgia-Pacific

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products/Services |

| 1 | Smurfit Westrock | Dublin | Ireland | World's largest corrugated and paper-based packaging company following the Smurfit Kappa-WestRock combination | Corrugated boxes, containerboard, retail packaging |

| 2 | International Paper | Memphis, Tennessee | USA | Global leader in containerboard and corrugated packaging manufacturing | Corrugated containers and shipping solutions |

| 3 | DS Smith | London, England | United Kingdom | Major European corrugated packaging producer with circular economy leadership | Corrugated packaging and recycling solutions |

| 4 | Mondi | Weybridge, England | United Kingdom | Leading integrated paper and corrugated packaging supplier | Corrugated packaging and containerboard |

| 5 | Packaging Corporation of America | Lake Forest, Illinois | USA | One of North America's largest corrugated packaging producers | Corrugated containers and displays |

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products/Services |

| 1 | Georgia-Pacific | Atlanta, Georgia | USA | Major North American corrugated packaging producer | Corrugated boxes and containerboard |

| 2 | Klabin | São Paulo | Brazil | Latin America's leading integrated paper and corrugated packaging company | Corrugated packaging solutions |

| 3 | Rengo | Osaka | Japan | Major Asian corrugated packaging supplier | Corrugated packaging and displays |

| 4 | Oji Holdings | Tokyo | Japan | Significant corrugated packaging operations across Asia | Corrugated containers and paper products |

| 5 | Saica Group | Zaragoza, Aragon | Spain | Leading European recycled paper and corrugated packaging company | Corrugated packaging and recycled containerboard |

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products/Services |

| 1 | VPK Group | Aalst, East Flanders | Belgium | Fast-growing European corrugated packaging specialist | Corrugated packaging and recycled paper |

| 2 | Model Group | Weinfelden, Thurgau | Switzerland | Regional leader in corrugated packaging innovation | Corrugated transport packaging |

| 3 | Carton Pack | Riese Pio X, Veneto | Italy | Specialized corrugated and food packaging supplier | Corrugated trays and food packaging |

| 4 | Fencor Packaging Group | Aylesford, Kent | United Kingdom | Independent corrugated packaging manufacturer | Custom corrugated packaging |

| 5 | Hinojosa Packaging Group | Xàtiva, Valencia | Spain | Growing European corrugated packaging producer | Sustainable corrugated packaging |

By Wall Type

By Packaging Type

By Application

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarCorrugated Packaging Market