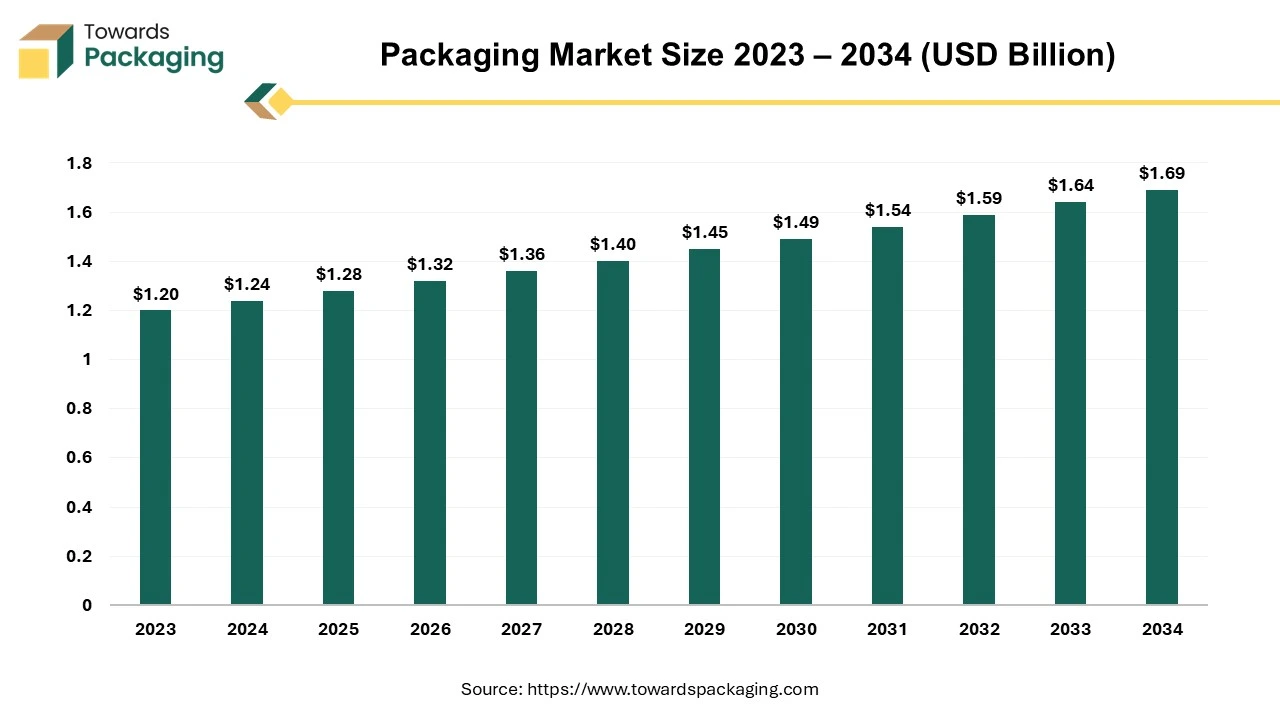

The global packaging market is forecasted to expand from USD 1.32 trillion in 2026 to USD 1.75 trillion by 2035, growing at a CAGR of 3.16% from 2026 to 2035. The Asia-Pacific region leads the market, with North America expected to grow significantly during the forecast period.

")

The paper & paperboard segment dominated the market, while rigid packaging holds the largest share in terms of packaging type. The flexography printing technology is leading the industry, and the food & beverages sector remains the primary end-user. Major companies such as Smurfit Kappa, Mondi PLC, and WestRock Company are actively contributing to market advancements.

Packaging is known as the process of designing, evaluating, and producing containers or wrappers for products. It plays a crucial role in protecting goods during storage, distribution, and sale. Packaging not only ensures the product reaches the consumer in good condition but also serves as a marketing tool, communicating brand identity and product information.

Packaging safeguards products from contamination, damage, and tampering during transportation, storage, and handling. It helps in preserving the quality and extending the shelf life of perishable items. Packaging facilitates ease of handling, storage, and usage of the product. It serves as a medium for conveying information such as usage instructions, nutritional information, and branding.

The packaging industry encompasses all businesses and activities involved in the design, production, and distribution of packaging materials and solutions. It is a vital sector in the global economy, supporting various industries like consumer goods, pharmaceuticals, food and beverage, cosmetics, and electronics. There is a significant push towards eco-friendly packaging solutions, including biodegradable materials, recyclable packaging, and minimalistic designs.

AI integration is revolutionizing the packaging market by enhancing efficiency, sustainability, and customer experience. AI can analyze vast amounts of data to develop optimized packaging designs that reduce material usage while maintaining structural integrity. Machine learning algorithms can quickly generate and test multiple design iterations, speeding up the prototyping process.

AI-powered sensors and analytics can predict equipment failures and maintenance needs, minimizing downtime and increasing productivity. Machine learning models can inspect packaging for defects or inconsistencies at high speeds, ensuring consistent quality. AI can recommend alternative, sustainable materials that reduce environmental impact without compromising quality. AI systems can monitor and optimize the use of resources, reducing waste during production and helping achieve sustainability goals. AI systems can monitor and optimize the use of resources, reducing waste during production and helping achieve sustainability goals.

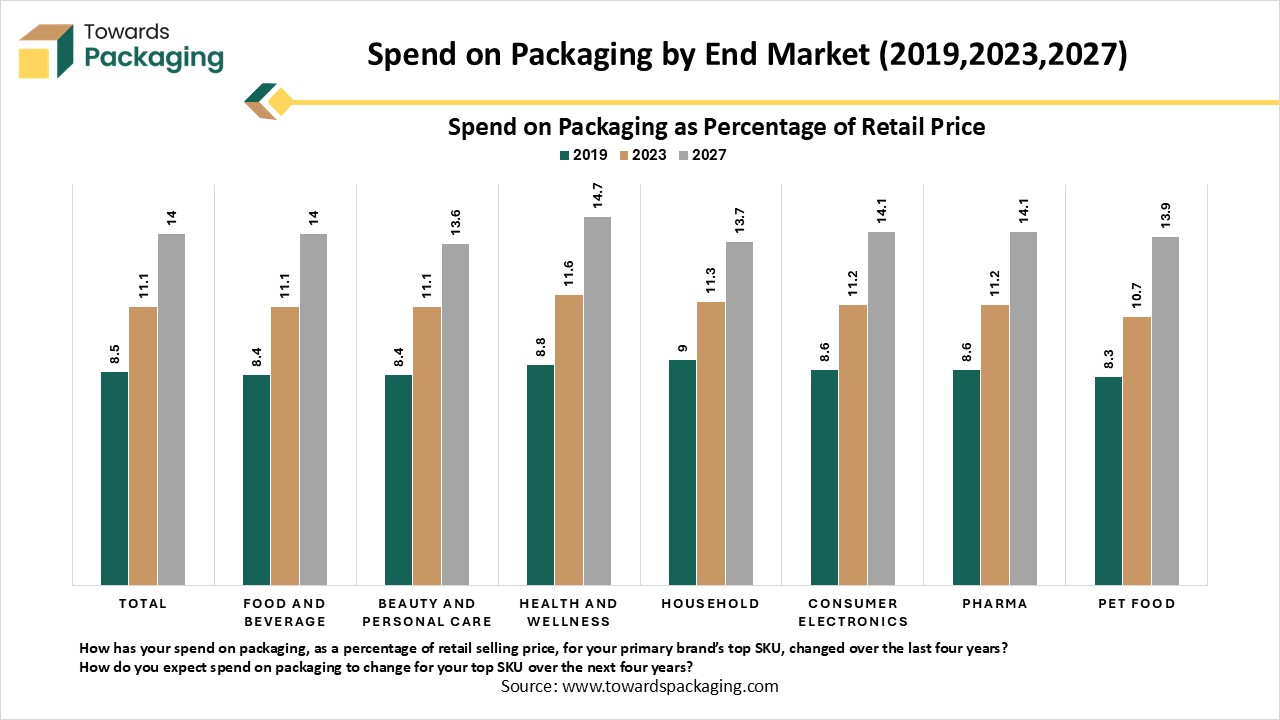

The chart shows how much companies in different industries spend on packaging as a percentage of the retail price of a product. It compares three years: 2019, 2023, and projected values for 2027. The eight end-market categories analyzed are:

")

Across every category, spending on packaging has been increasing from 2019 to 2023 and is expected to increase further by 2027. This means packaging has become a more important and more expensive part of delivering a product to the consumer likely due to sustainability requirements, rising material costs, improved packaging formats, and premiumization.

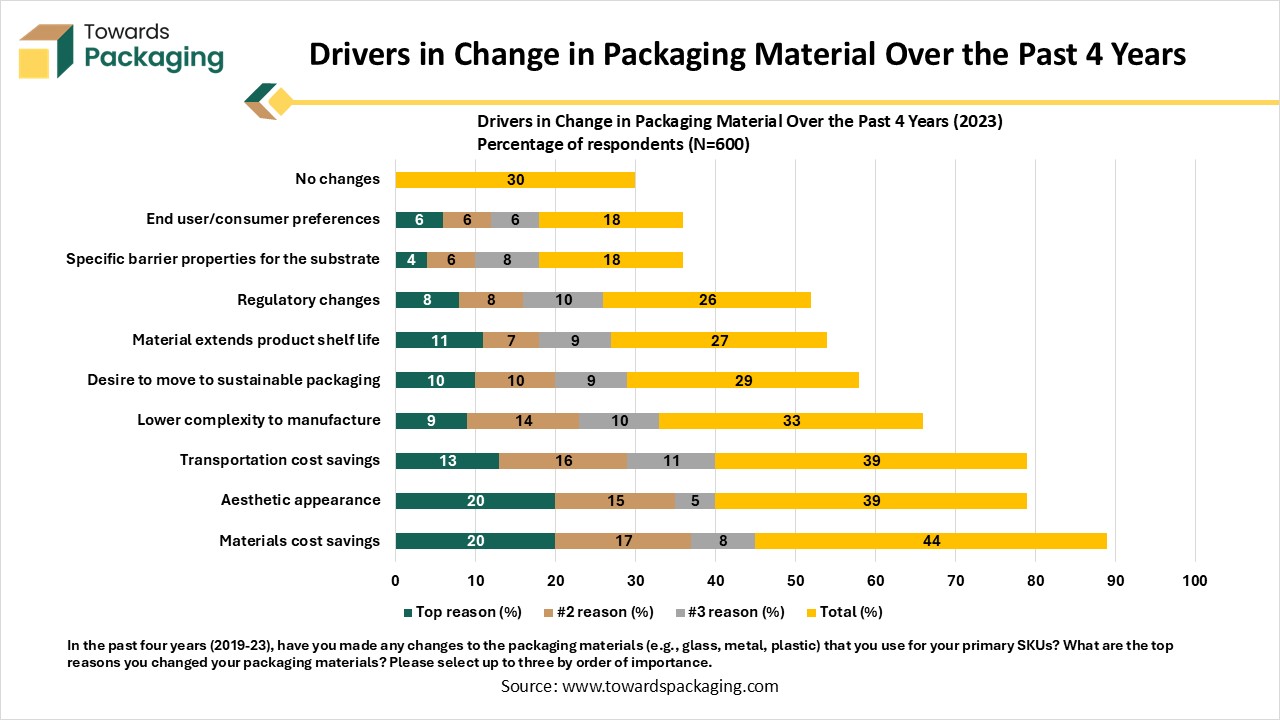

This chart shows the main reasons why companies changed their packaging materials over the last four years. The data is based on responses from 600 participants. Respondents were asked to select their top three reasons for making these changes.

The most common motivations for switching packaging materials are related to cost savings, sustainability, and appearance. These factors strongly influence packaging decisions across industries.

The last four years have seen a significant shift in packaging strategies. Companies are optimizing packaging to:

This shows that packaging decisions are increasingly strategic rather than purely operational.

")

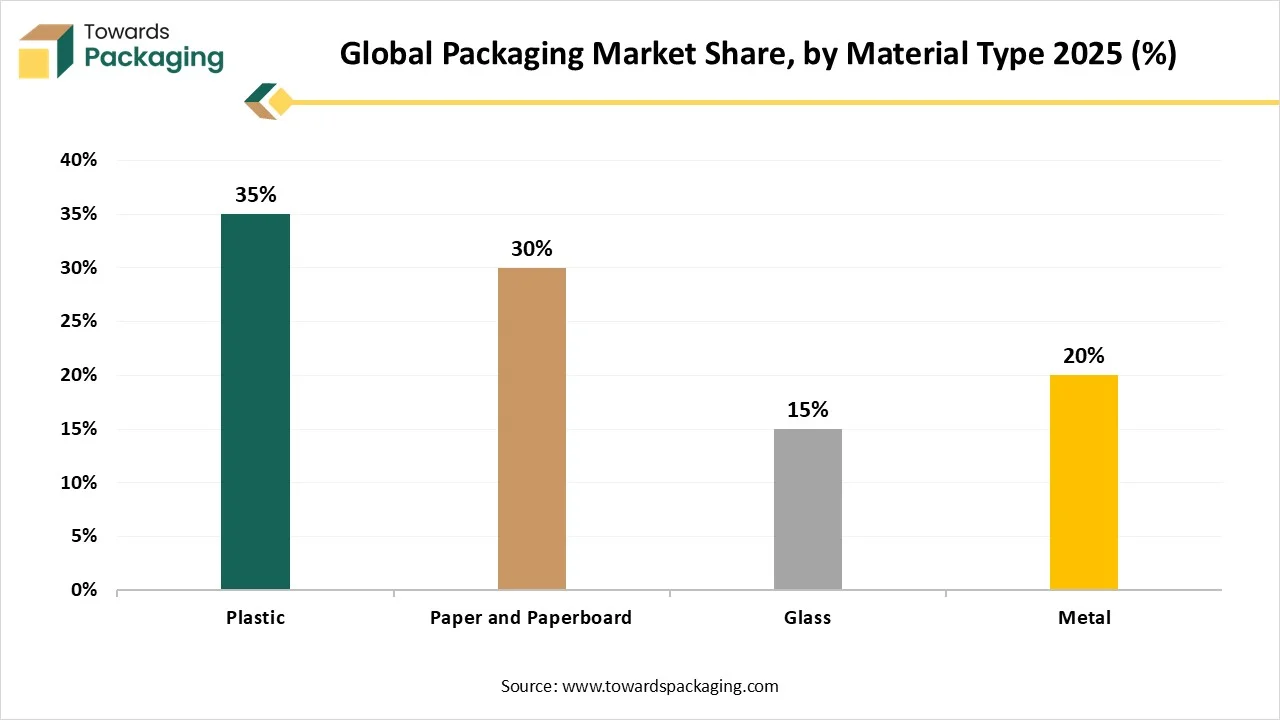

In 2025, the paper & paperboard market led the packaging market in 2025. Paper and paperboard are highly recyclable, which makes them more environmentally friendly compared to other materials like plastic. As sustainability becomes a growing concern, many companies and consumers are opting for paper-based packaging to reduce their environmental footprint. Paper and paperboard materials are generally less expensive to produce than alternatives like metals, glass, or plastics, which makes them an attractive choice for manufacturers.

As e-commerce continues to expand, the demand for corrugated boxes (a type of paperboard packaging) has surged. These boxes are essential for shipping and ensuring that products arrive safely at their destination. Governments and regulatory bodies worldwide are increasingly implementing policies to reduce plastic waste, which has spurred the shift to paper-based solutions. Many regions are now enforcing bans or restrictions on single-use plastics, and this has further fueled the growth of paper and paperboard packaging.

In 2025, the rigid packaging segment led the market with the largest share. Rigid packaging is highly durable and provides excellent protection for the contents, which is essential for a wide range of products, from food and beverages to pharmaceuticals and electronics. Its sturdiness helps prevent damage during transportation, handling, and storage. Rigid packaging also allows for complex designs, embossing, and color schemes that enhance brand visibility and appeal on retail shelves.

")

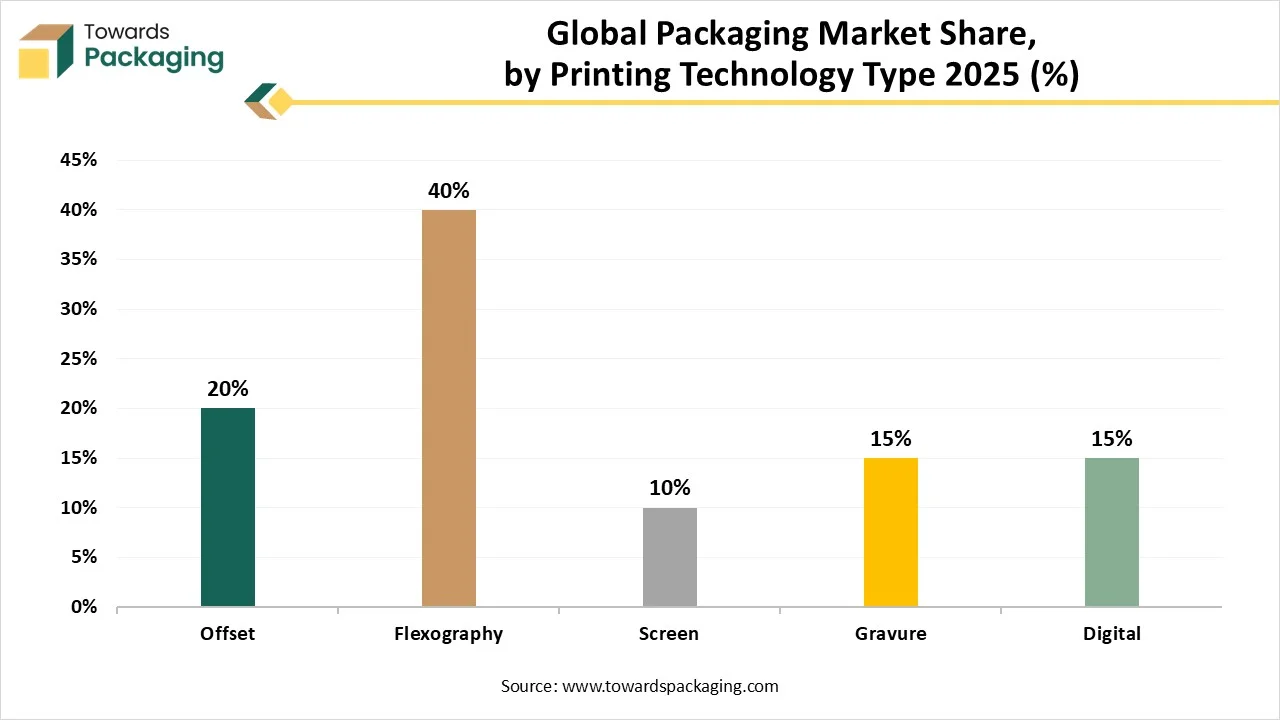

By printing technology, the flexography segment dominated the market. Flexography has become the preferred printing technology for industries such as food and beverage, pharmaceuticals, cosmetics, and consumer goods, all of which rely heavily on high-quality printed packaging. As flexible packaging continues to grow, due to its advantages in terms of lightweight, portability, and convenience, flexography remains the dominant printing method for these materials. Flexible packaging is popular in sectors like food and beverage (e.g., snack bags, beverage pouches), consumer goods (e.g., personal care packaging), and pharmaceuticals.

")

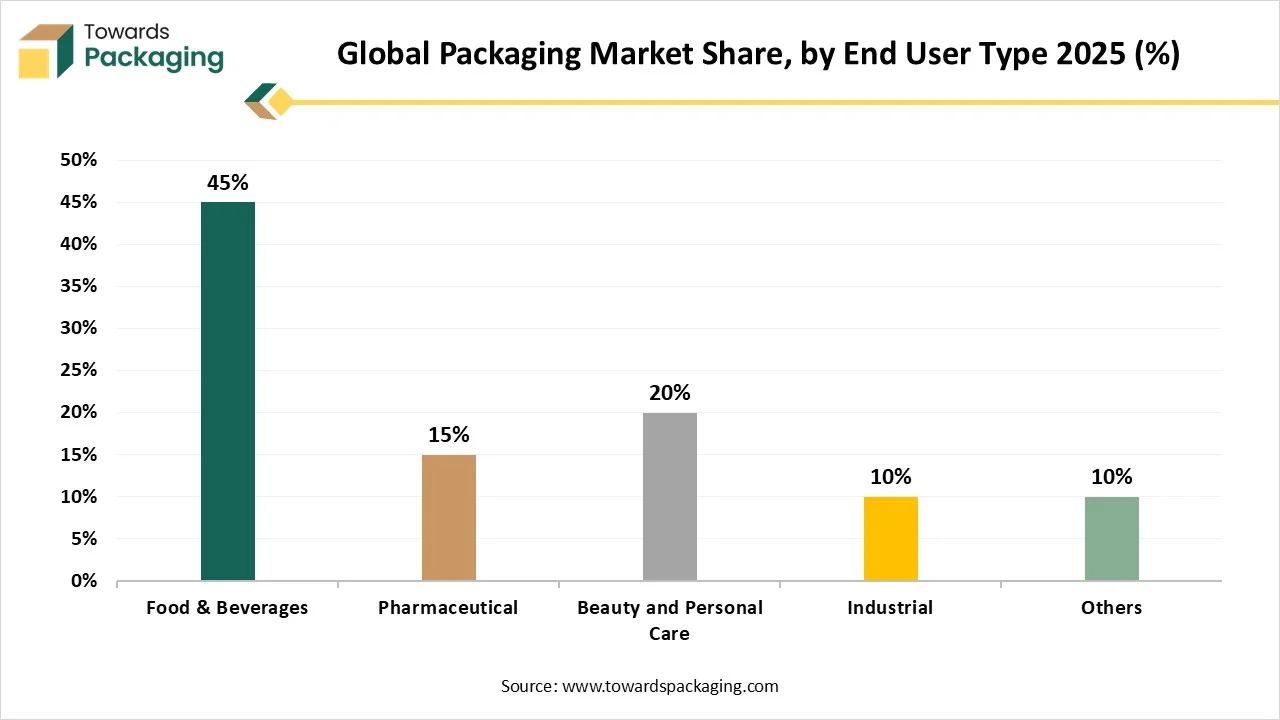

By end user, the food & beverages segment dominated the packaging market. With a rapidly growing global population and changing consumer lifestyles, there’s an ever-increasing demand for packaged food and drinks. Convenience, portion control, and longer shelf life are key trends that shape packaging needs. Glass bottles, plastic containers, metal cans, and jars are commonly used for beverages, sauces, dairy, and other food products. These materials are essential for preserving the quality and safety of the products.

Asia currently accounts for the majority of global packaging sales, owing to the rapid expansion of wealthier middle-class populations in developing countries such as China and India. This population change is followed by increased spending as revenues rise. The expansion of single-member households, an attraction for ready-to-eat meals and smaller container sizes, urbanization, and the increase in online shopping all help drive the growth of the packaging market in Asia. Global patterns in consumption are impacting the packaging business, with the Asia-Pacific area expected to develop at the most rapid pace.

| Material Category | 2025 Production | Installed Capacity |

| Paper & Paperboard | 132.14 million metric tons | 156 million metric tons |

| Plastic Products (total industrial output) | 76.97 million metric tons | 101 million metric tons |

| Primary Aluminum | 43.87 million metric tons | 51 million metric tons |

The leaders of this expansion are China and India. The primary consumer of sustainable packaging is the food and beverage industry, promptly followed by the personal care and cosmetics sector. Growing demand for eco-friendly products, increasing customer knowledge of environmental issues, and government programs supporting environmentally friendly packaging practices are all projected to contribute to the resilient development in sustainable packaging that the region of Asia-Pacific is expected to experience.

| Material Category | 2025 Production | Installed Capacity |

| Paper & Paperboard | 24.2 million metric tons | 32 million metric tons |

| Plastic Products | 19 million metric tons | 27 million metric tons |

| Primary Aluminum | 4.6 million metric tons | 4.8 million metric tons |

")

North America represents the globe's second-largest packaging market. The integrated markets of North America, consisting of the United States, Canada, and Mexico, account for a sizable percentage of the global packaging market. With an estimated revenue of 2,818 million euros in the United States alone by 2025. Though flexible packaging has reached commercial maturity in North America's industrialized nations, the outlook for future development is more muted. The United States appears as one of the fastest-growing packaging markets in the region. This expansion is being accelerated by the presence of major packaging businesses, such Amcor Ltd. and Mondi PLC, among others, which are supporting investments in R&D and innovation.

| Year | Total Packaging & Containers Waste (Million Short Tons) |

| 2023 | 82.2 MST |

| 2024 | 83.6 MST |

| 2025 | 85.1 MST |

Recycling Rate (2025): 55%

These companies play an important role in developing unique solutions to the market's different packaging difficulties. Their drive to push the boundaries of packaging technology ensures that the industry evolves indefinitely, fulfilling the ever-changing demands of consumers and businesses. The packaging industry in North America has an opportunity for continued expansion and adjustment owing to the strong foundation these industry leaders have laid. Innovation and appropriate investments will help the industry navigate the constantly shifting terrain of consumer preferences, legal requirements, and technology breakthroughs.

| Material Category | 2025 Production | Installed Capacity |

| Paper & Paperboard | 71.5 million metric tons | 78 million metric tons |

| Containerboard (corrugated base) | 40.2 million metric tons | 43 million metric tons |

| Plastic Resins | 122 million metric tons | 132 million metric tons |

| Primary Aluminum | 862 million metric tons | 1.9 million metric tons |

The European packaging market is rapidly expanding, with sustainability and environmental concerns taking primacy in all European countries. 74% of Europeans say that the problem of packaging waste has had a major impact on their purchasing decisions. Among European customers, more over half (52%) actively search out products packaged with eco-friendly materials; this percentage is significantly higher among French shoppers (55%) and Turkish shoppers (56%). Cardboard emerges as the preferred choice for eco-friendly packaging, with 52% of Europeans considering it is the most environmentally friendly material. This perspective is especially prominent in the UK, where 63% of consumers choose this material. Similarly, 45% of Europeans believe cardboard is the most recyclable material, followed by glass (32%). Tins/cans have the lowest perceived recyclability, behind only plastic marginally. The demand for protecting the environment has grown increasingly recognized across Europe.

"Easy to recycle" is ranked as the second preferred packaging feature, with 63% placing it in the top three. This is closely followed by the preference, which is highest among German consumers, for packaging composed of natural or renewable materials. As the European packaging market evolves, sustainable practices and environmentally friendly solutions are anticipated to remain important drivers of consumer preferences and industry developments.

| Year | Total Packaging Waste (Million Metric Tons) |

| 2023 | 84.3 MT |

| 2024 | 86.5 MT |

| 2025 | 88.2 MT |

Europe packaging market is driven by stringent sustainability laws, ambitious recycling goals, and rising consumer demand for environmentally friendly packaging designs. Owners of brands in the food, beverage, pharmaceutical, and personal care sectors are quickly moving towards packaging options that are lightweight recycllable and made of a single material. Flexible and intelligent packaging is still in high demand throughout the region thanks to technological advancements and established retail and e-commerce infrastructure.

Germany represents one of the most advanced packaging markets in Europe, backed by stringent waste management laws and a robust manufacturing foundation. The nation is a leader in the use of high-quality packaging designs, refill systems, and recyclable materials, especially in the food, automotive, and industrial packaging industries. Strong infrastructure for recycling and high consumer awareness both support market expansion.

| Material Category | 2025 Production | Installed Capacity |

| Paper & Paperboard | 22.4 million metric tons | 24 million metric tons |

| Packaging Paper Share | 56% of total output | - |

| Plastic Packaging Products | 15.2 million metric tons | 18 million metric tons |

The MEA packaging market is witnessing gradual expansion due to population expansion, urbanization, and rising packaged food and drink consumption. To cut down on plastic waste, governments in the area are implementing sustainability frameworks and promoting the use of recyclable and lightweight packaging. Packaging demand is also for retail and logistics infrastructure.

The UAE packaging market is growing steadily, fueled by robust demand from the pharmaceutical, food and beverage, and e-commerce industries. The use of recyclable and sustainable packaging materials is increasing as a result of government initiatives aimed at waste reduction and sustainability. The demand for superior long-lasting packaging solutions is further supported by the nation's position as a regional hub for trade and logistics.

The Latin America packaging market is supported by an increase in organized retail, middle-class consumption, and urban population growth. Due to their affordability and sustainability for food and personal care items, flexible packaging formats are becoming increasingly popular. Even though sustainability laws are still developing, growing environmental consciousness is promoting the slow adoption of recyclable packaging options.

Brazil dominates the Latin American packaging market due to its sizable consumer base and robust food, beverage, and agricultural sectors. Growing packaged food consumption and export activity are driving up demand for both rigid and flexible packaging. Further packaging innovations in the nation are anticipated to be shaped by a greater emphasis on recycling programs and circular economy practices.

| Rank | Company | Headquarters | Country | Key Packaging Segments |

| 1 | Amcor plc | Zurich | Switzerland | Flexible Packaging, Rigid Packaging, Healthcare Packaging |

| 2 | Smurfit Westrock | Dublin | Ireland | Corrugated Packaging, Consumer Packaging, Paper Packaging |

| 3 | International Paper | Memphis, Tennessee | USA | Containerboard, Corrugated Packaging |

| 4 | Mondi Group | Weybridge, England | United Kingdom | Flexible Packaging, Paper Packaging |

| 5 | Berry Global | Evansville, Indiana | USA | Rigid Plastic Packaging, Flexible Packaging |

Why Tier 1?

| Rank | Company | Headquarters | Country | Key Packaging Segments |

| 1 | DS Smith | London, England | United Kingdom | Corrugated Packaging, Retail Packaging |

| 2 | Sonoco Products Company | Hartsville, South Carolina | USA | Consumer Packaging, Industrial Packaging |

| 3 | Sealed Air Corporation | Charlotte, North Carolina | USA | Protective Packaging, Food Packaging |

| 4 | Stora Enso | Helsinki | Finland | Fiber-Based Packaging, Cartonboard |

| 5 | Oji Holdings Corporation | Tokyo | Japan | Paper Packaging, Corrugated Packaging |

Why Tier 2?

| Rank | Company | Headquarters | Country | Key Packaging Segments |

| 1 | Crown Holdings | Tampa, Florida | USA | Beverage Cans, Food Cans, Closures |

| 2 | Ball Corporation | Westminster, Colorado | USA | Aluminum Beverage Packaging |

| 3 | Verallia | Courbevoie | France | Glass Packaging |

| 4 | Ardagh Group | Luxembourg City | Luxembourg | Glass Packaging, Metal Packaging |

| 5 | Klöckner Pentaplast | Montabaur | Germany | Rigid Plastic Packaging, Food Packaging |

Why Tier 3?

North America

Europe

Asia-Pacific

Latin America

Middle East & Africa

By Material

By Packaging Type

By Printing Technology

By End User

By Region Covered

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarGlobal Packaging Market